Strategic Overview

Nicholas Levenstein & Company (NLC) operates at the intersection of institutional options pricing and retail market inefficiencies. Our mandate is to generate superior risk-adjusted returns by deploying capital where market data diverges from fundamental probability.

I. Crypto Money Fund Dollar Hedge II (CMFDH II)

Active StrategyThe CMFDH II strategy is a mature, multifaceted approach designed to capture yield through structural market conditions. It relies on the persistent volatility and interest rate differentials inherent in the digital asset ecosystem.

Visual Reference: Carry Trade Strategy

Core Mechanics

- Carry Trade: We capitalize on interest rate differentials between currency pairs. This targets an annual volatility of ~20% per unit.

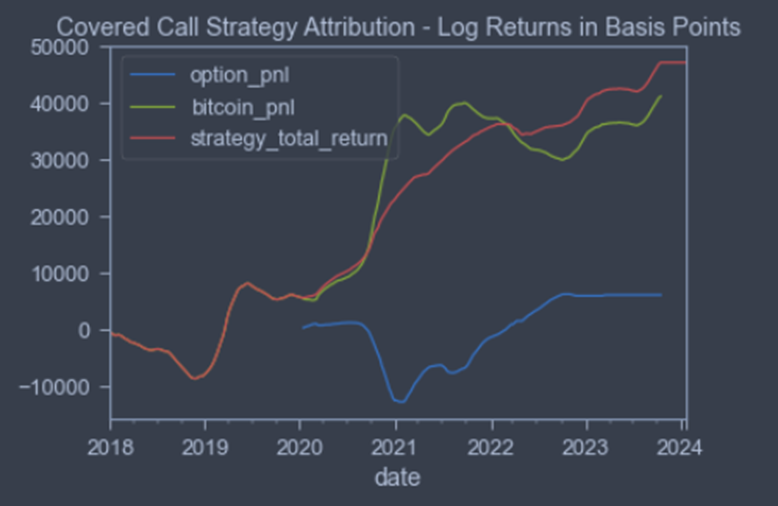

- Yield-Enhanced Covered Calls: We maintain long positions while systematically selling call options to capture the "volatility risk premium." This component targets ~40% annual volatility.

Architecture & Protection

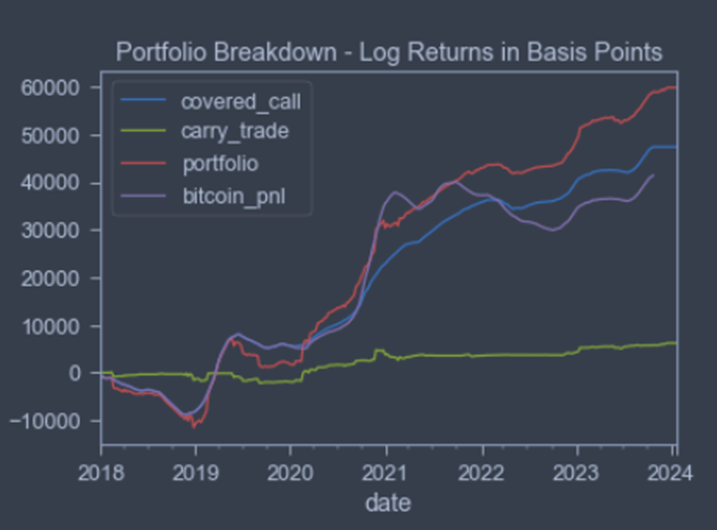

- Portfolio Construction: Allocated 50% to Contango strategies and up to 50% in Yield-Enhanced Covered Calls. Portfolio is rebalanced quarterly.

- The Contango Filter: We monitor contango yields against 90-day Treasury yields. Should contango fall below risk-free rates, we shift to cash to protect principal.

Call Strategy Dynamics

Portfolio Integration

II. Shadow Edge: Systematic Arbitrage

Options-Market Estimates vs. Prediction-Market Flow

The Thesis

Retail prediction markets like Polymarket often price intraday crypto outcomes based on sentiment. Conversely, institutional exchanges like Deribit price the same outcomes through professional volatility surfaces. Shadow Edge captures disagreement by taking the side of the more reliable institutional estimator.

Arithmetic Execution

Shadow Edge computes risk-neutral probability by differencing call deltas at the daily band boundaries on Deribit:

When this probability diverges from the Polymarket price by ≥ 5 percentage points, the strategy takes the favored position.

Why the Edge Persists

Polymarket participants systematically overpay for "wings" (extreme outcomes) and underpay at-the-money bands. This gap is measurable and arithmetic. The strategy observes where two markets disagree on the same probability and takes the more reliable side.

Risk Profile

No Leverage • No Overnight Exposure • Quarter-Kelly Sizing

Tracking

Real-time divergences are journaled via the Edge Tracker.

III. Executive Briefing: CMFDH II Strategy

Interview: Philippe Weberman with Nicholas Levenstein on the CMFDH II Strategy framework.